Watchdog News Global Economy Report

Gold, Oil, Debt, and War: What the Last 48 Hours Tell Us About the World Economy

By Jared W. Campbell — Watchdog News

Facts Over Factions

The Big Picture: The World Economy Just Flinched

The last 48 hours across global markets reveal a pattern that deserves a Watchdog eye.

Energy prices are surging.

Gold demand is rising again.

Stock markets are falling.

Currencies are shifting toward safe havens.

Bond yields are climbing across the world.

These signals rarely move together without a reason.

And right now, the reason is clear: war risk, inflation fears, and uncertainty about global economic stability.

When you step back from individual headlines and look at the broader pattern, the global financial system appears to be reacting to multiple pressures at once.

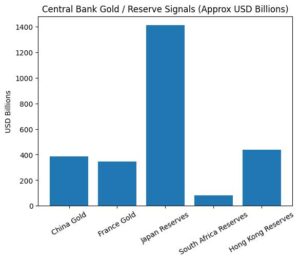

1. China Quietly Builds Financial Power

One of the most significant developments of the past two days received almost no mainstream attention.

China’s foreign exchange reserves have reached their highest level in more than a decade.

Key figures:

In total, reserves now stand at $3.428 trillion.

During the past month, reserves increased by $28.7 billion.

As a result, they have reached their highest level since November 2015.

At the same time, the People’s Bank of China has continued purchasing gold for 16 consecutive months.

China’s gold reserves now stand at:

• 74.22 million troy ounces

• $387.6 billion in value

China is not alone.

Other central banks are also expanding reserves or increasing gold exposure.

Examples include:

For example, France’s gold reserves have reached roughly €345.87 billion.

Similarly, South Africa has reported rising reserve assets, including gold.

Meanwhile, Switzerland has increased its gold holdings even as its foreign exchange reserves have declined.

In addition, Japan maintains a massive $1.41 trillion reserve portfolio that also includes substantial gold holdings.

Why This Matters

Central banks typically accumulate gold when they anticipate:

In particular, central banks are concerned about growing currency volatility.

At the same time, geopolitical instability is increasing uncertainty in global markets.

Meanwhile, inflation shocks remain a persistent risk for many economies.

In addition, policymakers are watching for signs of weakening in major reserve currencies.

The synchronized accumulation of reserves across multiple countries suggests system-wide hedging behavior.

In other words, central banks appear to be preparing for uncertainty.

2. Oil Shock Is Driving the Global Market Reaction

Energy markets have been among the most volatile sectors over the past week.

Oil prices have surged to their largest weekly rally since 2022.

Current benchmarks:

Meanwhile, WTI crude is trading near $90 per barrel. At the same time, Brent crude is approaching $91 per barrel. As a result, gasoline futures have risen to their highest levels since April 2024.

The cause is simple but significant.

The Strait of Hormuz — one of the world’s most critical energy chokepoints — has been partially disrupted.

Under normal conditions, the strait carries:

Approximately 20 million barrels of oil per day.

That represents around 20% of global petroleum trade.

Insurance costs for tankers have surged.

Shipping traffic has slowed.

Military tensions continue to escalate.

Some Gulf energy producers have warned they could halt production entirely if tanker traffic becomes unsafe.

Even the possibility of such disruptions is enough to trigger sharp reactions across global energy markets.

Geopolitical Shock Chain: Iran War-oil-inflation

3. Markets Are Reacting Like a Pre-Recession Environment

Financial markets responded immediately to the rising uncertainty.

Major global stock indices declined:

Meanwhile, the S&P 500 has fallen about 1.4 percent.

At the same time, the Nasdaq has dropped roughly 1.6 percent.

Likewise, the Dow Jones Industrial Average has declined about 1 percent.

Across the Atlantic, European markets are experiencing their worst week in months.

Meanwhile, Japanese equities have fallen more than 5 percent over the week.

This is classic risk-off behavior.

Investors typically shift money away from equities and into safer assets when they fear:

In particular, markets are increasingly worried about inflation.

At the same time, fears of a possible recession are growing.

Meanwhile, geopolitical escalation continues to add pressure to the global outlook.

At the moment, all three concerns are present simultaneously.

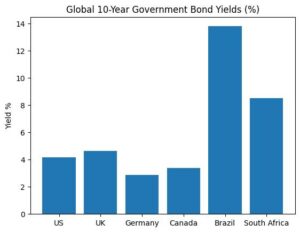

4. Bond Markets Are Signaling Inflation Risk

Across the world, government bond yields are rising sharply.

Rising yields typically signal that investors expect:

First, the risk of higher inflation is growing. Second, interest rates could remain elevated for longer than expected. Finally, fiscal risks for governments are beginning to increase.

Recent movements include:

United States

• 10-year Treasury yield around 4.17%, largest weekly increase since April

Canada

• 10-year yield approaching 3.4%

United Kingdom

• 10-year gilt yield near 4.62%

Germany

• Bund yield reaching a four-week high

Brazil

• 10-year yield above 13.8%

South Africa

• 10-year yield around 8.5%

Bond markets tend to react faster than political systems.

Their message appears clear: inflation risk is returning.

Global Government 10 Year Bond Yield %

5. The U.S. Economy Is Sending Mixed Signals

Economic indicators from the United States add another layer of uncertainty.

Key data points:

Labor Market

• 92,000 jobs lost in February

• unemployment rose to 4.4%

Retail Activity

• retail sales declined 0.2%

Consumer Credit

• Borrowing growth slowed significantly

Wages

• wages continue rising 3.8% annually

At the same time:

Meanwhile, energy prices are climbing. At the same time, supply chains face rising geopolitical risk. As a result, inflation expectations are moving higher.

This creates a troubling combination.

Economists often describe it as stagflation risk:

Meanwhile, economic growth is slowing. At the same time, prices are rising. In addition, labor markets are starting to weaken.

Central banks have limited tools when those forces appear simultaneously.

Central Bank Gold/ Reserve Signals

6. Inflation Is Uneven Around the World

Global inflation is no longer moving in a single direction.

Instead, it has become highly fragmented.

Inflation Rising:

For example, inflation pressures are rising in Colombia. Meanwhile, El Salvador is also seeing higher prices. At the same time, Vietnam is experiencing inflationary pressure. Similarly, Taiwan is facing rising inflation.

Inflation Stable

• South Korea

• Switzerland

Inflation Falling

Meanwhile, inflation pressures are easing in Chile. At the same time, Costa Rica is also seeing prices moderate. Similarly, inflation is beginning to fall in Mauritius.

Extreme Inflation

• Venezuela — 617% annual inflation

This uneven pattern suggests the global economy is entering a divergent phase, where different regions face very different economic pressures.

7. Gold Is Quietly Reasserting Itself

Gold has continued climbing as investors seek safety.

Prices are now trading near record levels above $5,100 per ounce.

Three major forces are driving demand:

1️⃣ geopolitical instability

2️⃣ inflation concerns

3️⃣ central bank accumulation

Historically, extended periods of central bank gold buying have often occurred during times of global monetary uncertainty.

8. Commodity Markets Signal Supply Pressure

Commodity markets are showing early signs of inflationary pressure spreading through supply chains.

Recent price increases include the following:

For example, cocoa prices have climbed about 5–6 percent. Meanwhile, wheat prices are up roughly 4–5 percent. In addition, silver has gained about 2 percent. Most notably, oil prices have surged nearly 12 percent in a single week.

Meanwhile, the FAO Food Price Index has risen to a four-month high.

Food inflation often follows energy inflation for several reasons:

First, higher energy prices push fertilizer costs upward. Second, transportation becomes more expensive as fuel costs rise. Finally, agricultural inputs across the supply chain become more costly

Historically, food price spikes have contributed to political instability in developing regions.

9. Manufacturing and Industrial Data Show Weakness

Industrial activity in several regions has weakened.

Examples include:

Argentina

industrial production down 3.2%

Hungary

industrial output down 2.5%

Croatia

manufacturing production declining

Norway

industrial output weakening

Romania

GDP growth has been the weakest since 2021

At the same time, some economies continue expanding, including Latvia, Georgia, and Greece.

This divergence further reinforces the picture of a fragmented global recovery.

10. Safe-Haven Capital Is Moving

Periods of uncertainty often trigger shifts in global capital flows.

Countries perceived as politically stable or geographically insulated can attract investment.

One recent example:

New Zealand has reopened luxury real estate markets to foreign investors, targeting global wealth seeking stable assets and long-term security.

This trend reflects a broader movement of capital toward perceived safe havens.

The Watchdog View

When a Watchdog examines global events, the goal is not to chase headlines.

It is to look for patterns.

Across the last 48 hours, several signals align:

Meanwhile, China and several other central banks are increasing their gold holdings and foreign reserves.

At the same time, oil markets are beginning to price in the risk of a potential supply shock.

Globally, bond yields are rising as investors reassess risk and inflation expectations.

Meanwhile, stock markets are moving in the opposite direction and showing signs of decline.

As a result, safe-haven currencies and assets are gaining strength.

At the same time, inflation fears are returning while economic data continues to weaken.

No single indicator proves a global shift.

But when multiple signals move in the same direction, it suggests the system may be under strain.

The Iran war may be the immediate trigger.

But the deeper issue may be something larger:

A global economy that has been operating for years on fragile supply chains, high debt levels, and growing geopolitical tension.

Major economic turning points rarely arrive with a single dramatic announcement.

They usually begin with dozens of smaller signals moving quietly in the same direction.

Right now, those signals are moving.

And a Watchdog would be wise to keep watching.

Jared W. Campbell- Watchdog News

Facts over Factions