Global Markets Reprice Risk as Iran War Escalates

Global Markets Flinch, Then Reprice: The Iran War Enters a More Complicated Economic Phase

Monday, March 16, 2026

By Jared W. Campbell — Watchdog News

👁 Facts Over Factions

The past 26 hours have hardly brought the calm we hoped for; instead, they’ve unleashed a more insidious threat: a fleeting sense of relief amid a crisis that continues to escalate.

This distinction is crucial.

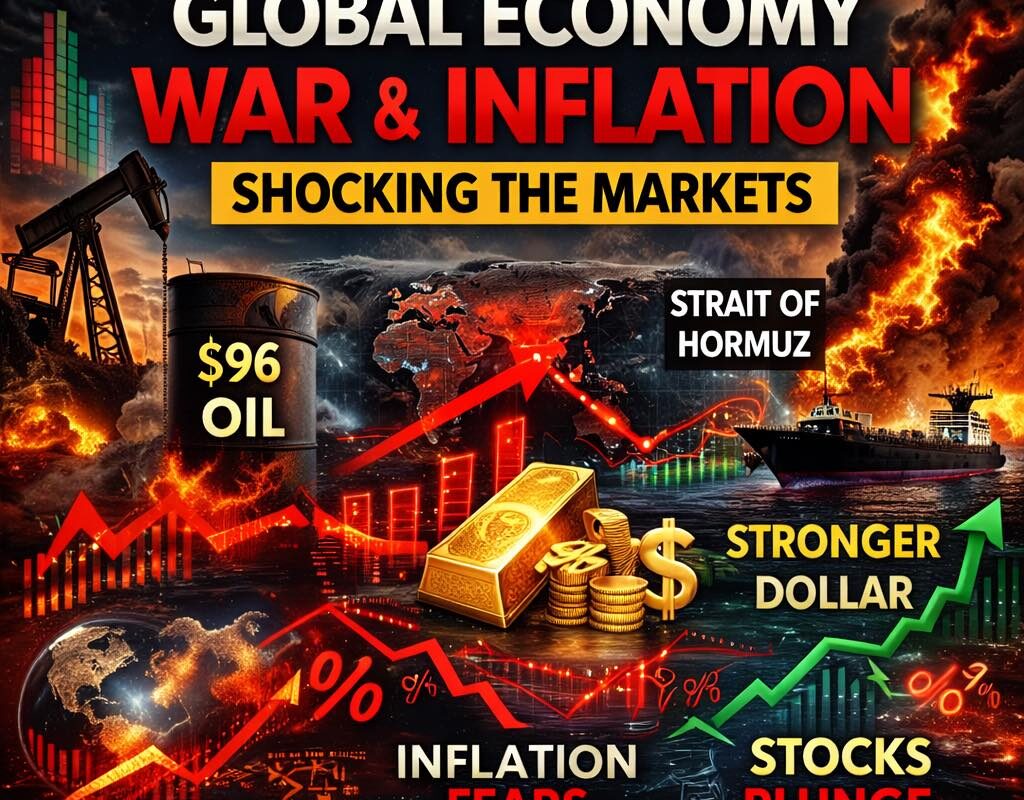

As markets kicked off the week, we saw a modest rebound driven by tankers successfully navigating the Strait of Hormuz and by Washington’s hint of temporary leeway for Iranian oil shipments. Traders started to entertain the notion that the strait might not remain entirely off-limits after all. Yet, the overall landscape is anything but stable. Brent crude clung to prices above $100, while WTI momentarily crossed that same threshold before retreating slightly. Heating oil and gasoline remain near multi-year highs, and European gas prices rose once more. Central banks now find themselves grappling with a new inflation conundrum layered atop slowing growth and mounting geopolitical tensions.

In Asia, there was a glimmer of hope as China’s activity data for January and February surpassed expectations, providing some support for the markets, despite a rise in unemployment and ongoing struggles in the property sector.

The market message: not de-escalation, but recalibration

What happened Monday was not a clean “risk-on” move. It was a recalibration.

European stocks rebounded, with the STOXX 50 and STOXX 600 up, while Germany’s DAX recovered and U.S. equities bounced from near four-month lows. Canada’s TSX stabilized, Brazil’s Ibovespa jumped, and India’s Sensex snapped a losing streak. But those gains came alongside oil still elevated, the euro still weak, gilt and Bund yields still high, and investors still bracing for policy decisions from the Fed, ECB, BOE, BOJ, RBA, Bank Indonesia, and others. In other words, markets were not saying the danger had passed. They were saying the worst-case shipping shock may have softened slightly — for now.

Strait of Hormuz: the center of gravity is still maritime

The most important theme is unchanged: the Strait of Hormuz remains the economic center of gravity of this war.

My observation matters because the WTI fell more than 3% intraday, to around $95, after some vessels passed through the chokepoint. At the same time, other reports still had WTI and Brent near or above $100 after the weekend’s strikes at Kharg Island and renewed threats to energy infrastructure. That is not a contradiction. That is, volatility is driven by one question: can enough shipping move to prevent a full energy shock? Reuters separately reported that Japan has no current plan to join a Hormuz escort mission, underscoring that even U.S. allies are carefully weighing the military and legal risks.

The Watchdog takeaway is this: Iran may not need a perfect blockade to pressure the world economy. A partial choke, selective passage for aligned or tolerated ships, repeated attacks near ports like Fujairah, and enough uncertainty to slow insurers, reroute traffic, and freeze decision-making can still function like an energy weapon. That is one of the biggest things many people miss. The war does not need a total closure to inflict global costs.

Oil eased, but the inflation problem did not.

This morning, we see that Brent is above $100 and WTI is near the mid-90s to low-100s, still representing a major inflationary problem, even after Monday’s partial pullback. Heating oil remained above $4 per gallon and gasoline around $3.08, both near highs not seen since 2022. European natural gas rose toward €52/MWh, while UK gas also stayed elevated. Aluminum hovered near four-year highs after production cuts in Bahrain, and copper remained under pressure from a stronger dollar and weaker property demand in China. All of those points point to something bigger than oil alone: the war is pushing a wider raw-material and transport-cost shock through the system.

That is why the phrase “oil fell today” can be misleading. Yes, crude pulled back from panic highs. But the broader signal is still inflationary. Markets are not pricing peace. They are pricing disrupted energy with intermittent relief.

Central banks are now trapped between war, inflation, and weakening growth.

This is where the Watchdog’s report stands out.

The major economic pattern is not just “oil up, stocks down.” It is that central banks are being forced into a narrower corridor of choices.

In the U.S., Treasury yields eased modestly on Monday, but the 10-year remained near 4.24%-4.25%, and markets still price only one Fed cut, likely late in the year. Manufacturing output and industrial production both beat expectations, capacity utilization held steady, and homebuilder sentiment edged up, but the New York manufacturing survey stalled badly. That combination suggests the U.S. economy is not collapsing, yet it is not cleanly accelerating either. Add war-driven energy costs, and you get a stagflation risk the Fed cannot ignore.

In Europe, the problem is sharper. The euro stayed near seven-month lows, Bund yields held near two-year highs, UK gilt yields remained above 4.7%, and money markets are now pricing ECB tightening far more aggressively than before the war shock intensified. Europe is more exposed to disruptions in imported energy than the United States, so every extra dollar in crude and every extra spike in LNG or marine insurance costs carry outsized consequences.

In Australia, yields are near 2011 highs and markets are leaning toward another RBA hike. In Japan, policymakers are facing a weak yen and rising import inflation, but Reuters reports that Tokyo has no immediate plan to send warships into the Hormuz Strait. That illustrates the tension: highly energy-dependent economies want the route open, but not all are eager to militarize their response.

Here is a video that covers quickly from March 9-13, 2026- Watchdog Accuracy check: ~8.5/10. The video summary is broadly accurate. Its five main economic claims — U.S. CPI up 0.3% in February, the U.S. trade deficit narrowing to $54.5 billion in January, German exports falling 2.3%, Japan revising Q4 GDP growth up to 1.3% annualized, and China’s exports rising 21.8% in January–February — all align with contemporaneous reporting. The main limitation is that it relies on a summary news source rather than primary statistical releases.

North America: relief rally, but not reassurance

The U.S. rebound was driven by a reduction in immediate energy panic, lower Treasury yields, and renewed enthusiasm in tech and AI names like Nvidia and Micron. Canada also benefited from softer February inflation at 1.8%, lower bond yields, and a stronger loonie. But neither market looks structurally safe.

Canada still has a rising unemployment rate, major job losses, and a softening domestic economy. The TSX rebound suggests investors welcome the immediate easing of the oil panic, not that Canada has escaped global stress. In the United States, the stock market rebound says something similar: traders are buying a pause, not a solution. That is a very different thing.

Europe: rebound on screens, pressure underneath

European equities bounced on Monday, but underneath the surface, the region still looks fragile.

The DAX gained on corporate news, reducing immediate energy-related fear. The STOXX benchmarks rose. The FTSE tried to recover. UniCredit’s on Commerzbank lifted banking stocks. But Europe also remains squeezed by high energy prices, weak currency dynamics, and rising rate expectations. Italy’s MIB still lagged. The eurozone’s vulnerability to another imported energy shock remains one of the most underappreciated risks in the global economy.

Asia: not one story, but several

Asia did not move as a unified bloc.

China’s data for January and February exceeded expectations for industrial output, retail sales, and fixed investment, benefiting Hong Kong and boosting regional sentiment. However, unemployment rose to 5.3%, and new home prices fell at the fastest rate in eight months. This highlights a significant internal imbalance in China. While there is stronger state-supported activity on one hand, there is still weakness in the property market and labor sector on the other.

In India, some relief came from the safe passage of LPG carriers and successful diplomacy with Tehran, which helped stocks recover. However, the trade deficit widened sharply, the rupee remained close to record lows, and wholesale inflation reached a one-year high. India exemplifies how a country can demonstrate resilience while being highly vulnerable to external oil shocks.

Japan’s market remained cautious, with the yen slightly strengthening amid fears of government intervention, while bond yields edged higher. According to Reuters, Prime Minister Takaichi stated that Japan is not currently planning a Hormuz escort mission. This is strategically important, as it suggests that one of the world’s energy-dependent economies is still aiming to avoid direct military entanglement, despite increasing economic exposure.

Southeast Asia faced the typical challenges of net energy importers. Indonesia’s rupiah weakened towards 17,000, its stock market dropped to an eight-month low, and Bank Indonesia began a policy meeting under inflationary pressure. The Philippine peso approached 60, prompting central bank intervention, while South Korea’s currency hovered near levels seen during past crises, even as chip stocks provided occasional boosts to the KOSPI. These are the types of currency stresses that arise when the global market begins to reprice oil risk faster than domestic policymakers can adequately respond.

Latin America: rebound with inflation anxiety still alive

Brazil’s spav jumped nearly 2%, helped by lower intraday oil prices, stronger January activity data, and a general global recovery bid. But Focus bulletin expectations for 2026 inflation and the Selic rate both moved higher. That matters. Brazil’s sket can rally on relief, but policymakers are still staring at the possibility of imported inflation through fuel, freight, and fertilizer channels.

Mexico’s also strengthened in parts of Monday trading, but that should not be mistaken for insulation. The broader emerging-market picture remains split between temporary rebound flows and long-term vulnerability to oil-driven inflation, dollar dynamics, and trade-route disruption.

Commodities beyond crude: the deeper inflation web

Here is another place where the Watchdog flow can outclass routine market coverage.

The inflation threat is not only crude oil. It is also:

European gas, UK gas, heating oil, gasoline, aluminum, shipping premiums, freight uncertainty, and agricultural knock-on effects. Soybeans fell amid U.S.-China uncertainty, palm oil extended gains on stronger demand and possible Indonesian tax changes, and steel held up amid a decline in Chinese output. These are not isolated commodity stories. They are the outlines of a broader system in which war simultaneously affects energy, fertilizer, transport, metals, manufacturing inputs, and food costs.

That is how regional wars become global cost-of-living events.

A coalition may calm shipping — or widen the war.

The Watchdog connection, as noted in my notes, is the coalition question.

Multiple reports suggest that Washington is pushing toward an escort coalition for vessels transiting the Strait of Hormuz, while Europe is discussing expanding its naval missions, and some Asian governments remain cautious. Reuters’ report that Japan is not currently planning an escort mission is important because it shows that alliance unity is not automatic. If a coalition forms, it may stabilize shipping. But it could also further militarize the chokepoint, increasing the risk of miscalculation.

So the same development, sold to markets as a stabilizer, may also carry the seeds of a wider confrontation. That is classic Watchdog terrain: the solution and the escalation can be part of the same move.

The Watchdog view

Here is the clearest way to read Monday:

The world transitioned not from crisis to calm, but from panic pricing to conditional repricing.

Some tankers crossed. Oil eased from its highs. Stocks rebounded. Yields slipped. Yet, the deeper challenges persist:

The Strait of Hormuz is the most perilous economic chokepoint on the planet right now.

Central banks are navigating the pressures of energy-led inflation.

Major importers in Asia remain exposed.

Europe still faces the potential of renewed energy strain.

The coalition question can either stabilize trade or extend the conflict.

And the market grapples with the most profound question of all: how long will this war last?

This is the pattern many overlook.

When you connect these dots, the signal is not that the global economy is secure. The signal is that the global economy is engaged in a war that has evolved into both a military conflict and an economic stress test.

And that is why Monday is significant.

Because it serves as a reminder that, even amid moments of relief, we are very much aware of the greater challenges that lie ahead.

Jared W Campbell- Watchdog News

👁 Facts Over Factions