Few places on earth have the power to shake the global economy faster than the Strait of Hormuz.

Oil, War, Weak Growth, and the World’s Most Dangerous Chokepoint

By Jared W. Campbell — Watchdog News

March 13, 2026:

👁 Facts Over Factions

Over the last 23 hours, the global economy has continued to send the same warning in multiple languages: this war is no longer just a military event. It is an energy shock, an inflation shock, a market shock, and potentially the beginning of a much larger geopolitical fracture.

That is the pattern I see when I step back from the daily spot reporting.

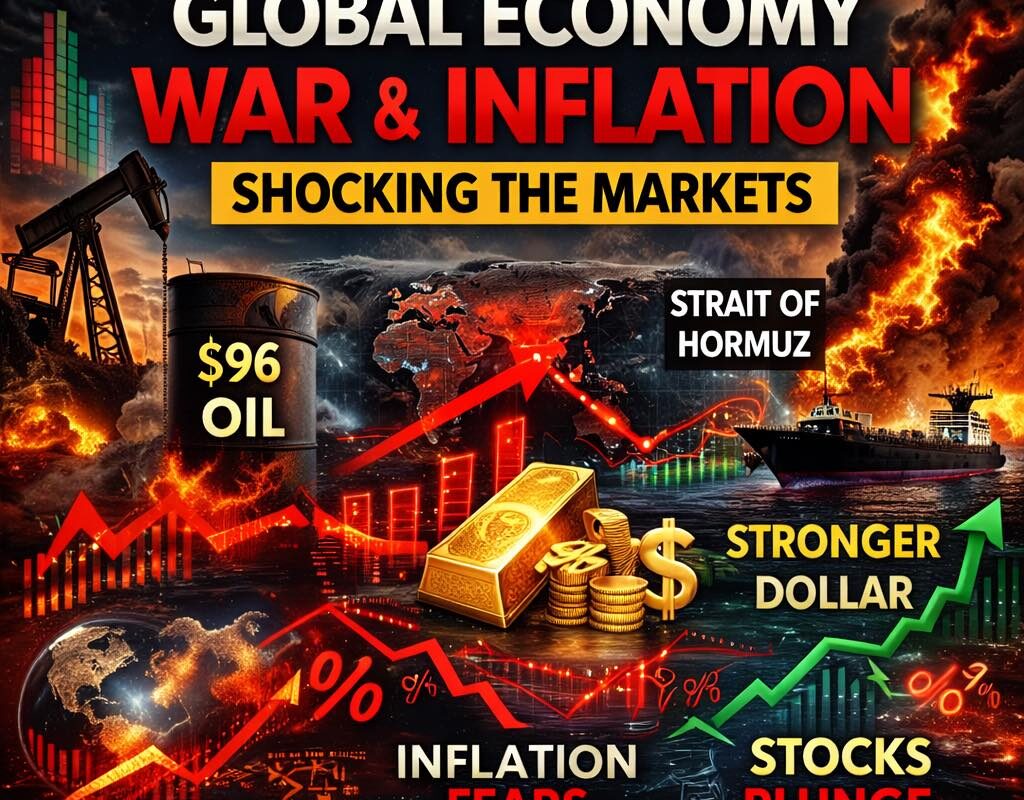

The Strait of Hormuz remains the center of gravity. Reuters reported today that this is now the largest oil supply disruption on record, with roughly 8 million barrels per day, or about 8% of global supply, affected, prompting the IEA and member nations to approve a record 400 million barrels to be released from reserves. Reuters also reported that Saudi Arabia has already sharply cut output, with total Gulf-region production losses reaching at least 10 million barrels per day as maritime disruption spreads.

https://www.reuters.com/business/energy/biggest-global-oil-supply-disruptions-history-2026-03-13/

That helps explain why my market notes are so important.

Oil is still holding near crisis territory. WTI pushed above $96, and Brent has repeatedly traded around or above $100, even after the largest strategic reserve release in IEA history and even after Washington temporarily eased sanctions on some stranded Russian cargoes. Reuters also reported Goldman Sachs has raised its March Brent outlook to above $100 a barrel, while warning that a prolonged disruption could keep prices structurally higher later in the year.

Few places on earth have the power to shake the global economy faster than the Strait of Hormuz.

https://www.reuters.com/business/energy/biggest-global-oil-supply-disruptions-history-2026-03-13/

That is the backdrop for everything else in your notes.

The dollar index climbed above 100, its highest level since last spring, as investors sought safety. U.S. 10-year yields remained elevated around 4.25% to 4.27%, reflecting persistent concern over energy-driven inflation and war spending. The FTSE 100 ended the week lower on weak UK growth and Middle East tensions. The DAX stayed under pressure. European stock benchmarks were down around 1%. India posted one of its sharpest weekly losses in years. Hong Kong and mainland China also struggled. Canada, Brazil, and Mexico all reflected the same basic problem: war is now being priced through energy, inflation, rates, and weaker confidence.

The U.S. data added another layer of concern.

Headline PCE inflation eased to 2.8%, but core PCE accelerated to 3.1%, still well above the Fed’s target. At the same time, U.S. GDP growth for Q4 2025 was sharply revised lower to 0.7%, and consumer sentiment fell to 55.5, with survey officials explicitly linking the weaker sentiment to the conflict with Iran and rising gasoline prices. In other words, the United States is now staring at the dangerous mix that markets hate most: slower growth, still-sticky inflation, and rising energy costs.

That is why the word stagflation keeps hanging over these markets.

This is not yet a full 1970s-style global stagflation spiral, but the ingredients are there. Reuters, AP, and other reporting over the last several days all point to the same stress points: energy supply disruption, maritime insecurity, delayed monetary easing, and weakening consumer confidence. AP also reported that pro-Iranian cyber actors are widening their attacks into U.S. and regional targets, which means this conflict is no longer just about bombs and missiles. It is increasingly economic, digital, logistical, and psychological.

That is where the Watchdog has to slow down and ask the harder questions.

How close are we to World War III?

My objective answer is this: closer than people want to admit, but not there yet.

This is already a major regional war with global economic consequences. It involves the United States, Israel, Iran, Gulf shipping, global energy markets, cyber escalation, and mounting great-power tension around sanctions, oil flows, and maritime security. Reuters reported Germany is already rebuking Washington’s temporary Russian oil waiver, and broader diplomatic friction is building as states weigh energy stabilization against the wider Ukraine conflict. AP is warning of broader cyber spillover. That is not a world war, but rather an overlapping crisis environment in which larger wars become possible through miscalculation.

https://www.theguardian.com/world/2026/mar/13/iran-war-oil-prices-russian-sanctions-lifted

A real-world war would mean direct, sustained military intervention by multiple major powers on opposing sides. We are not there. But we are on a dangerous escalation ladder: oil shocks, proxy attacks, cyber operations, maritime disruption, great-power friction, and a real risk of misreading intent.

That is not peace. That is pre-expansion territory.

Will America survive if this war with Iran drags on?

Yes, America will survive.

But that does not mean America would emerge from a long war undamaged.

The United States has greater structural resilience than most countries in this crisis because it is more energy-independent than Europe or many Asian importers, and markets still treat the dollar as the main haven. That is one reason the dollar is strengthening even while U.S. growth data weakens. But survival and strength are not the same thing. A long war would mean higher deficits, higher interest burdens, deeper domestic political divisions, growing cyber vulnerabilities, and a greater risk that Americans would once again pay strategic costs far beyond what they were initially told.

So yes, America survives.

But a drawn-out war could still weaken the country economically, fiscally, politically, and psychologically.

Will Israel and Iran survive?

My view is this: both are likely to survive as states, but they could take heavy losses.

Israel is clearly taking damage, even if the public picture is incomplete. Earlier Reuters-linked reporting and other international coverage have documented the impacts of Iranian strikes in places like Rehovot and the Tel Aviv area. At the same time, outside analysts have repeatedly noted that Israeli military censorship limits the full public visibility of impact sites and damage assessments. At the same time, Reuters reported today that Israel is still intensifying internal operations against IRGC and Basij-linked infrastructure inside Iran, and there is still no clear sign that the war has produced regime collapse or organized internal overthrow.

The video below is from an Iranian missile strike in Israel.

Iran is also absorbing heavy damage and pressure. ACLED’s latest special issue says strikes have hit hundreds of locations across at least 26 of Iran’s 31 provinces, including missile infrastructure, naval assets, air defenses, leadership facilities, and internal security sites. But ACLED also makes clear that Iran’s political and coercive apparatus remains active, meaning this is not a clean collapse scenario.

https://acleddata.com/update/middle-east-special-issue-march-2026

That is the deeper point many people keep missing.

This war does not yet look like a fast regime-ending campaign. It looks more like a grinding attritional conflict where both sides can keep inflicting punishment while neither side secures the kind of decisive political end state that headlines keep promising.

So yes, Israel and Iran likely survive.

But “survive” may come with severe military, economic, infrastructural, and civilian losses.

What Happens to the Global Economy If This Continues?

That depends on duration.

If this remains a short-lived disruption, the world economy may emerge with a severe but temporary inflation shock, slower growth, and another round of central bank caution.

If it lasts longer, the risks rise dramatically.

The immediate path is already visible, and my notes reflect that Europe is vulnerable due to LNG disruptions, energy dependence, and renewed expectations of ECB tightening. European natural gas remains far above its start-of-month levels, even with somewhat lower day-to-day volatility, because QatarEnergy halted operations, and UAE-linked LNG routing has also been disrupted. Europe has alternatives through rising U.S. LNG output and investment, but those alternatives are not frictionless or instant.

Asia is vulnerable because it is more dependent on imported fuel, shipping continuity, and manufacturing margins. South Korea’s won is near crisis-era lows. Japan is confronting weak yen inflation and fears of intervention. India has seen huge foreign outflows and one of its worst weekly stock declines in years. China is holding up somewhat better than many expected because it spent years building strategic reserves and diversifying energy exposure. However, its credit data still show underlying weakness, with new yuan loans declining for an eighth straight year-over-year reading.

Emerging markets are especially exposed. Brazil is battling high yields and fertilizer risk. Mexico is facing a weaker peso and diminished room for rate cuts. The Philippines just posted its highest jobless rate since mid-2022. Canada’s labor market weakened sharply, with employment down 83,900 and unemployment up to 6.7%, while factory sales and capacity utilization both softened. These are the kinds of secondary stresses that show the war is no longer confined to regional economic effects.

Even commodity markets are sending mixed but useful signals. Oil, heating oil, gasoline, and coal all surged on supply fears. Wheat, cotton, wool, and palm oil showed selective gains. Gold failed to act as an unstoppable crisis asset because a stronger dollar and higher yields capped it, even as China kept buying. Silver and platinum weakened at points for the same reason. The Baltic Dry Index, meanwhile, continued climbing and posted a weekly gain, suggesting global shipping stress is not just theoretical.

That is why I would frame the global economy this way:

Right now, it is not collapsing.

But it is being repriced.

The market is shifting toward a world of higher energy costs, higher geopolitical risk premiums, fewer near-term rate cuts, weaker growth, and deeper vulnerability in countries that depend on imported fuel and stable shipping lanes.

If Hormuz remains functionally closed or heavily restricted, and if attacks spread across shipping, cyber networks, and regional bases, then the global economy moves from inflation scare into full-blown systemic stress.

The Watchdog View

A lot of reporting right now still feels too narrow.

One article talks about oil. Meanwhile, another focuses on stocks. Elsewhere, reports examine missiles and diplomacy. However, the real story emerges when all of these threads are viewed together.

That pattern is now unmistakable.

The U.S.–Israel war with Iran has become the center of gravity for a global repricing of risk. Oil remains elevated. Shipping remains impaired. Natural gas remains unstable. Bond markets are pushing back against rate-cut dreams. Equities are struggling to believe in a soft landing. Safe-haven flows are flooding into the dollar. And major economies are increasingly being divided into those that can absorb the shock and those that cannot.

So, how close are we to World War III?

Not there yet.

But close enough that dismissing the possibility would be foolish.

Will America survive?

Yes. But a long war could still leave deep scars.

Will Israel and Iran survive?

Likely yes. But survival may come at a devastating price for both.

What happens to the global economy?

That depends on whether this shock breaks quickly or becomes the new normal.

And that is the real Watchdog warning tonight:

The greatest danger may not be one dramatic headline.

It may be the slow realization that the world economy, global trade system, and regional security order are all being tested at the same time.

Jared W. Campbell

👁 Facts Over Factions